Is the mini-correction in markets a foretaste of something bigger, or does the still-strong real economy give risk assets scope to bounce back?

Should investors be rotating out of equities and into bonds, or are the latter still vulnerable to buyers' strikes against a backdrop of fiscal indiscipline?

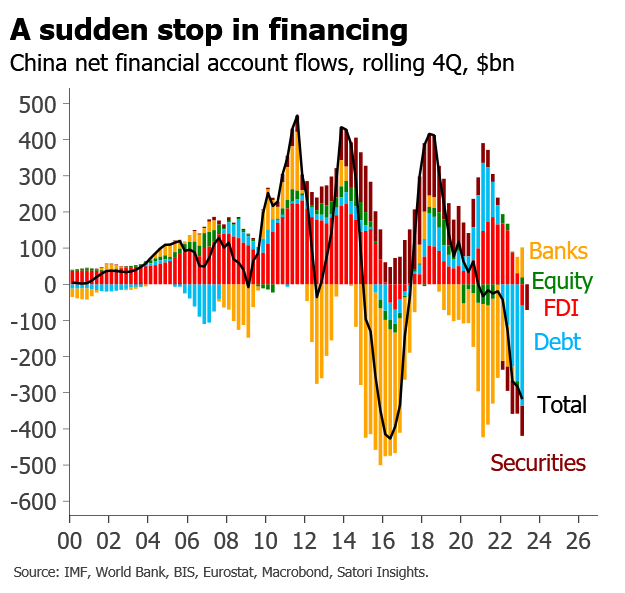

Net capital outflows from China have accelerated sharply in recent months

They are now running at a near-2015 rate

The only real source of 'inflows' is a drop in prior foreign lending by domestic banks as they divert capital onshore - but even this can be interpreted as a sign of vulnerability