In a narrow technical sense, the FOMC was indeed hawkish

But in the cessation of QT and through questions, it more broadly reconfirmed a reaction function at once deeply asymmetric and completely oblivious to asset price inflation

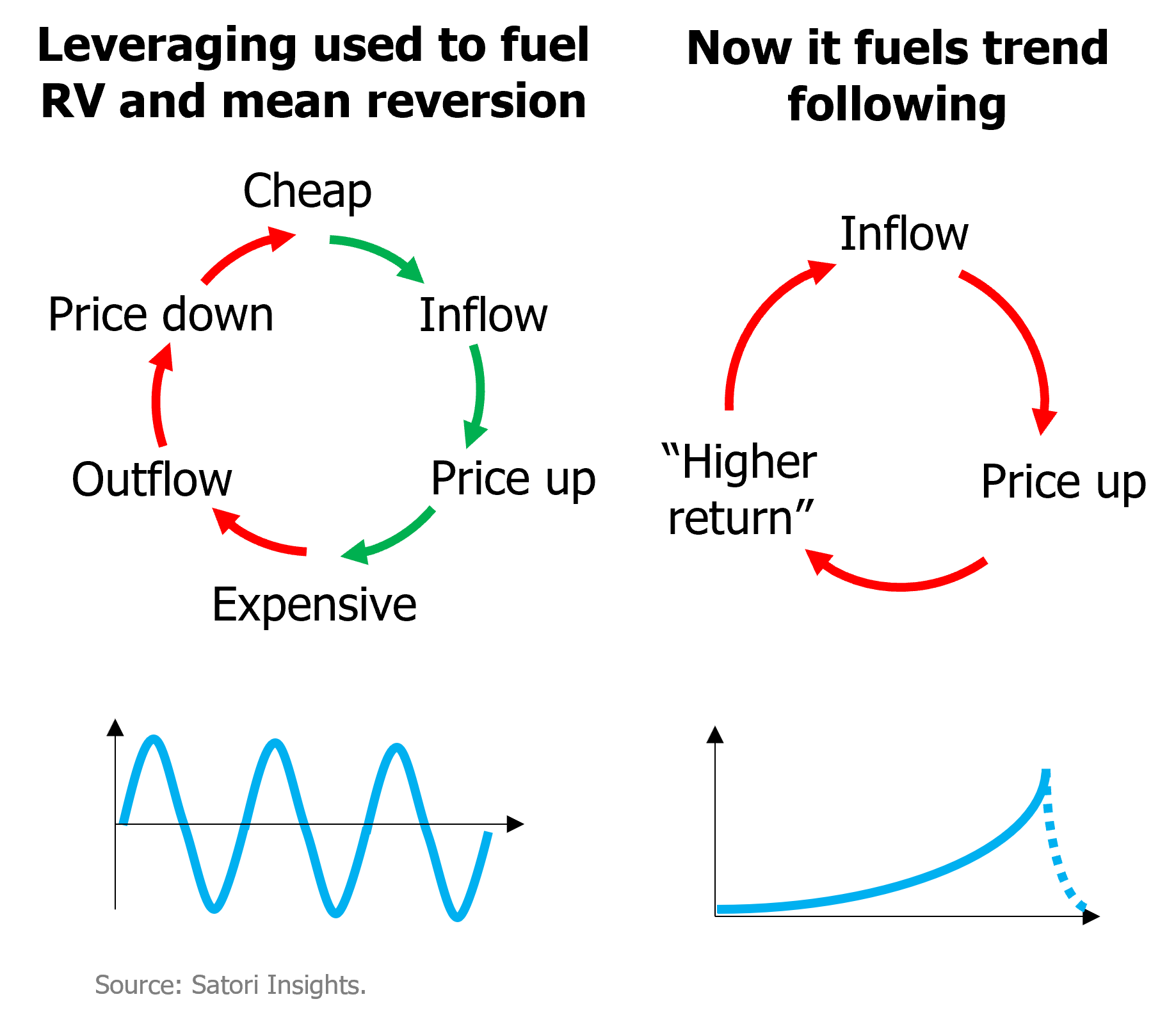

This paves the way for a further melt-up in risk assets and havens - and for more assets to exhibit the sort of exponential sawtooth boom-bust recently seen in gold

The single greatest force driving modern economies, society and politics is scalability

It is the common narrative underlying the dominance of big tech, through to the teen mental health crisis and the rise of political polarization and populism

Markets tend to treat scale as a largely linear concept

But human systems change character at scale - and ultimately have breaking points

Clients with Group Webinar or One-on-One subscriptions should log in to see the full version

The single greatest force driving modern economies, society and politics is scalability

It is the common narrative underlying the dominance of big tech, through to the teen mental health crisis and the rise of political polarization and populism

Markets tend to treat scale as a largely linear concept

But human systems change character at scale - and ultimately have breaking points