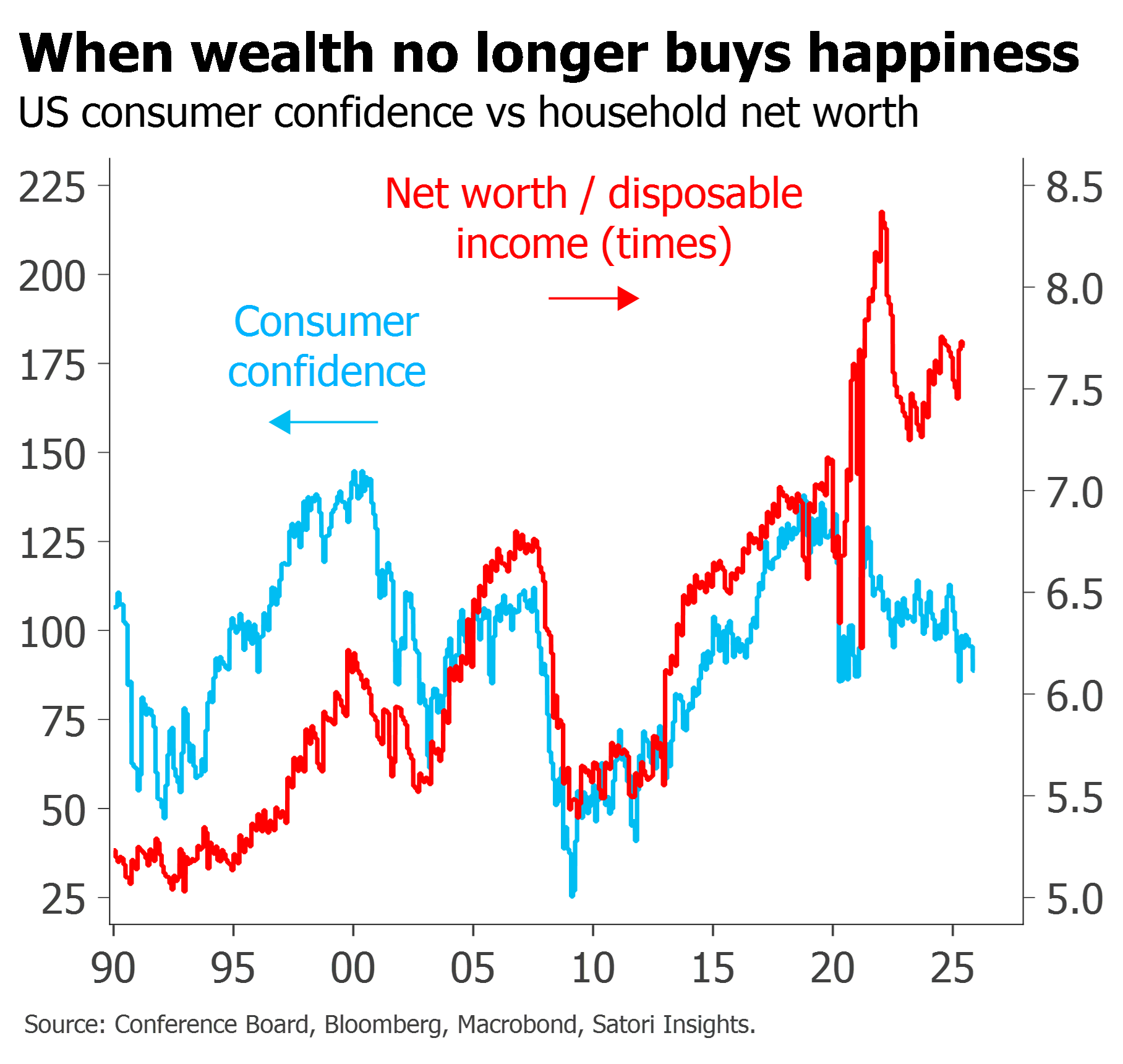

The more markets rise, the greater is the gap to consumer sentiment

We are used to explaining this in terms of a K-shaped economy

But together with record profit share and margins and the narrowness of the equity rally, it is also consistent with monopolization, regulatory capture and enshittification

This helps explain why not only labour but also consumers are suffering, implies a critical role for politics - and ultimately paints a more fragile picture of society collapsing towards technofeudalism

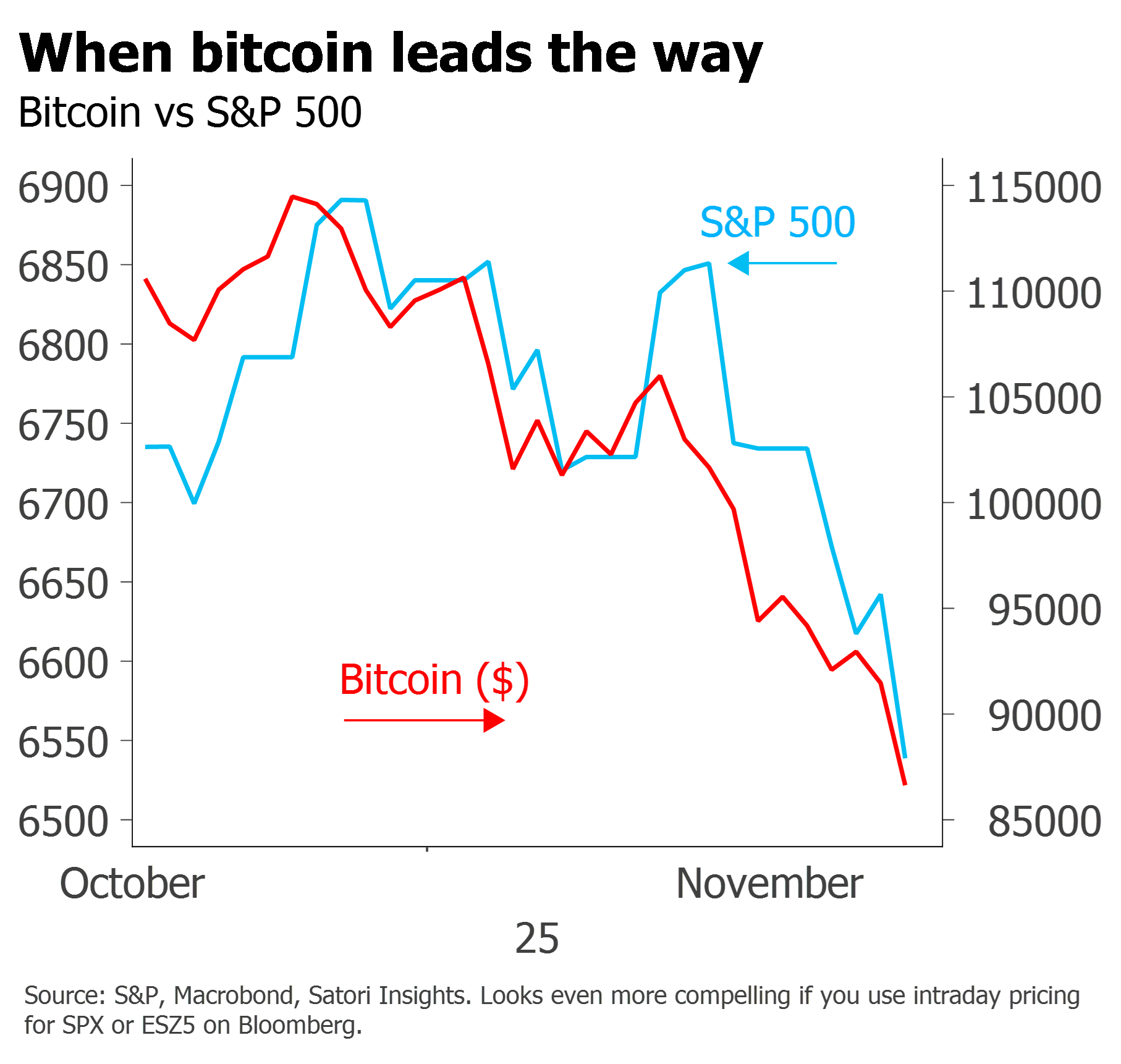

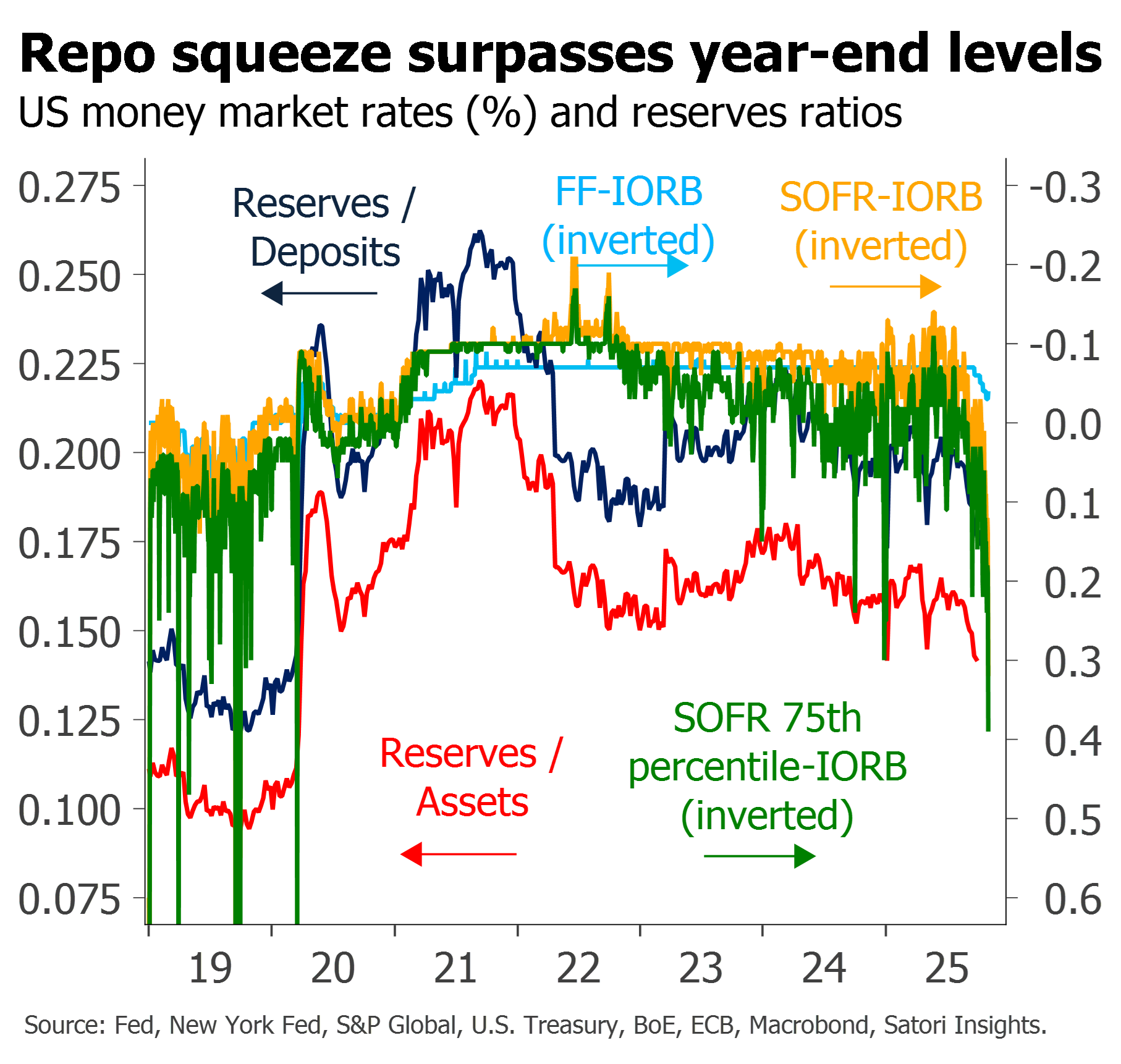

Markets are reeling from a monetary triple whammy: repo tightness, a faltering of other forms of credit creation, and a record $900bn in reserves drainage

But all these sources of monetary tightness ought to ease

The question is whether this episode drives a more enduring reduction in risk appetite and fund flows