Skip to content

- The latest central bank research on QT is careful, rigorous, and grounded in the literature

- Unfortunately its main conclusion – that QE affects markets while QT doesn’t – is at odds with the lived experience of most market participants

- There is a much simpler reason why QT has had so little apparent impact

- Misunderstanding of this dynamic greatly contributes to the likelihood of future policy mistakes

- Free-to-view replay of first segment of 16 Jan webinar

- Why strategists struggled in 2023

- A better way to think about markets

- Implications for 2024

- Hark! The VC angels sing

- God rest ye, merry crypto bros

- While PMs watched tech stocks take flight

- I’m dreaming of a tight market

- To be sung, please, in a spirit of global harmony

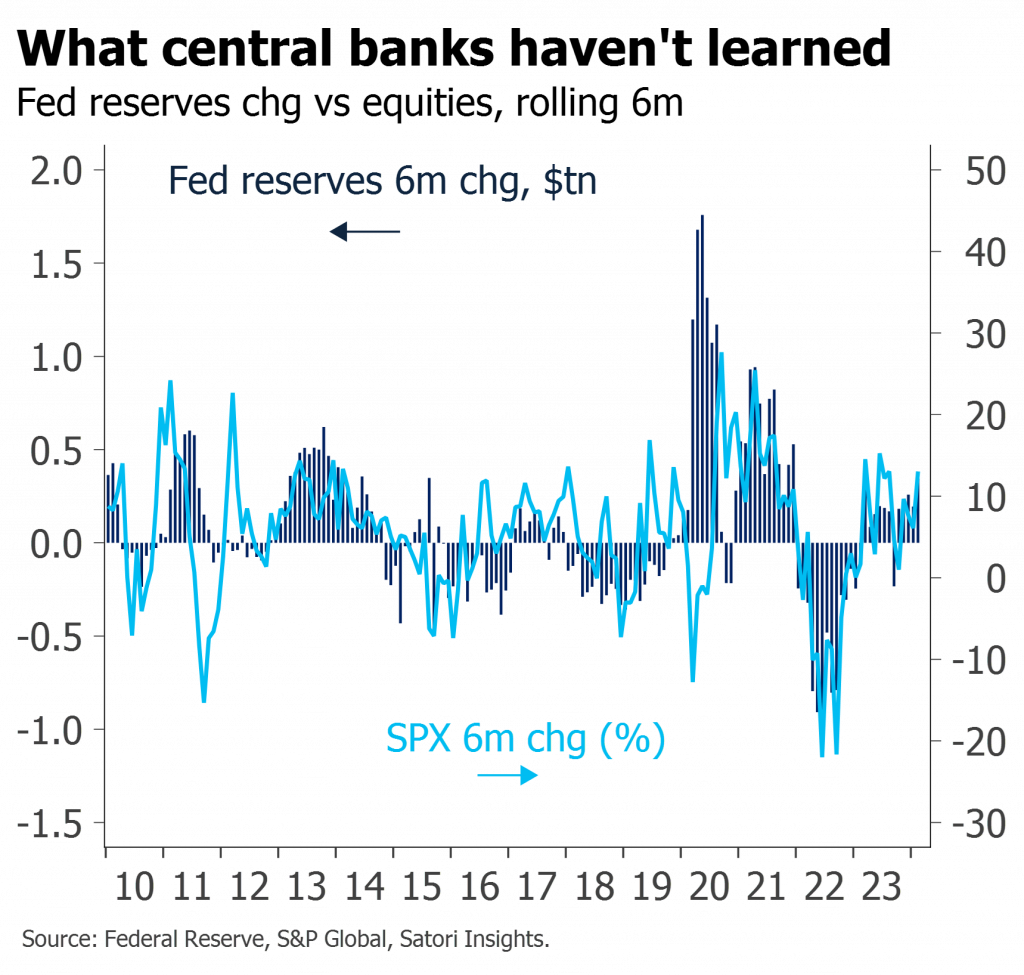

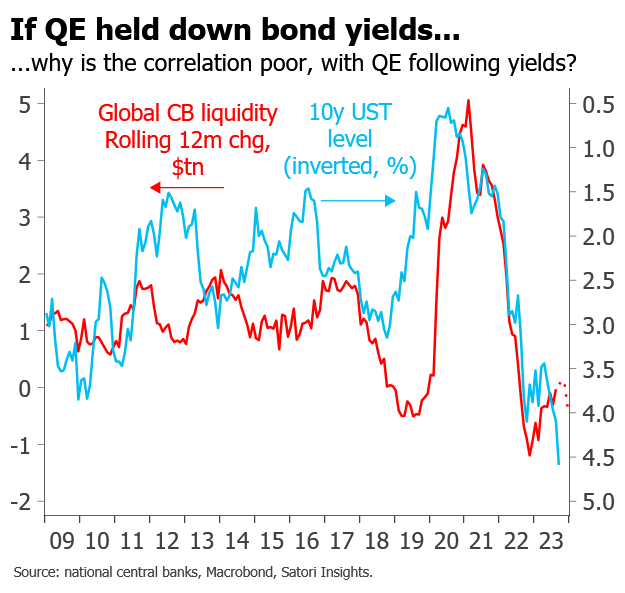

- It is often said that QE held down bond yields, meaning QT should be a major contributor to this year’s rise

- But the evidence for this is deeply questionable

- QE does indeed hold down real yields, through a portfolio balance effect

- But it also pushes up inflation breakevens via signalling

- What is missing so far from this round of QT is the historical fall in breakevens

- The true driver of higher bond yields lies with inflation, not QT