Skip to content

The outlook for AI continues to dominate markets

But the best insights come from first-hand experience

This piece is free to view

Free clip from 28 Apr webinar

From oil above $120 to a Fed Chair who can’t trust a “closed” investigation, short term is driven by war and whim

But the slide towards lawlessness is structural — not just Trump, not just populists

Investors keep wanting to assume continuity in a world where the rules themselves have become negotiable

First 15 minutes free to view; full version only for clients with Group Webinar and One-on-one subscriptions

Free clip from 23 Jan webinar

Consensus around 2026 forecasts is completely at odds with real-world uncertainty

The trick for investors is finding ways to position for underpriced regime change risks without simply disinvesting

First 15 minutes free to view; full version only for clients with Group Webinar and One-on-one subscriptions

Free clip from 22 Oct webinar

The fuel for the rally comes from a mix of fiscal stimulus being channelled into fund flows and financial sector leveraging

But cracks are beginning to appear, from First Brands, to doubts about circular financing in tech, to the flight into gold

To understand the limits of leveraging, look at the fund flows

First ten minutes free to view; full webinar only for clients with Group Webinar and One-on-one subscriptions

Free clip from 8 Jul webinar

The single greatest force driving modern economies, society and politics is scalability

It is the common narrative underlying the dominance of big tech, through to the teen mental health crisis and the rise of political polarization and populism

Markets tend to treat scale as a largely linear concept

But human systems change character at scale – and ultimately have breaking points

Clients with Group Webinar or One-on-One subscriptions should log in to see the full version

Free excerpt from 11 Apr webinar

It’s not just that tariffs are still not priced

The increasingly alarming price action in Treasuries and the $ threatens to take down other markets

Clients with One-on-One or Group Webinar subscriptions should log in to see the full replay

Free excerpt from 22 Jan webinar

The US economy is indeed exceptional

But the performance of its markets owes just as much to an extraordinary funnelling of fund flows

Dissecting the drivers of these flows sheds crucial light on the durability or otherwise of the risk rally

Free to view by all; full replay available only to clients with Group Webinar or One-on-One subscriptions

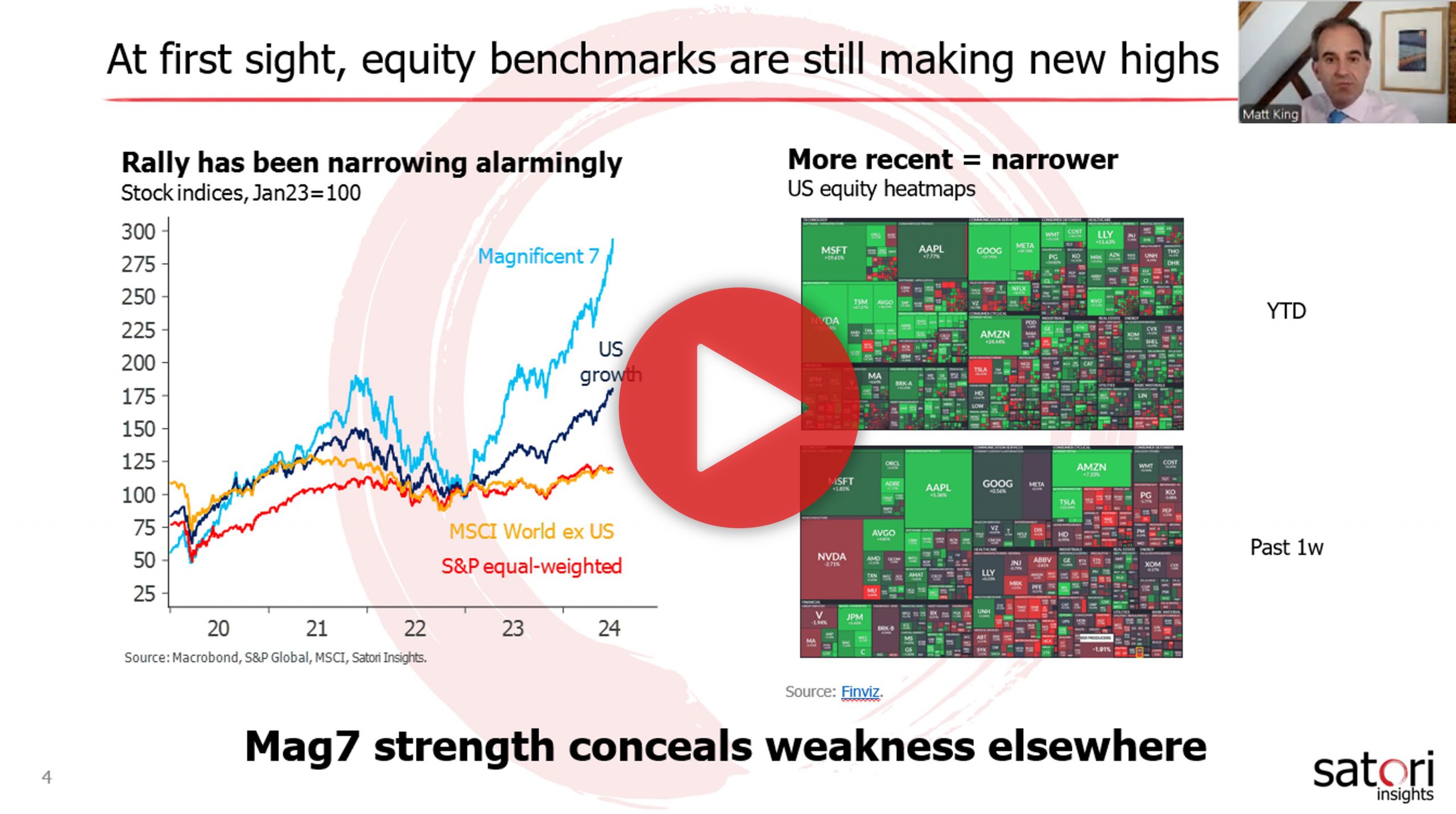

A chart of publication titles against price action

Free excerpt from 16 Oct webinar

Markets’ aggressive pricing of a soft landing is matched only by central banks’ determination to provide it

Yet their dovishness masks a switch from rate tightening and balance sheet easing to rate easing and balance sheet tightening

The resultant uncertainty is largely reflected in rates – but leaves opportunities in other markets

Available to all; full replay available only to clients with Group Webinar or One-on-One subscriptions.

Free clip from first ten minutes of 3 July webinar

Even as the rally continues, it does so on ever more fragile foundations

The problem lies neither with the economy, nor with central banks being slow to lower rates, nor even with politics

It is that the liquidity which fuelled markets in H1 looks increasingly likely to be turned off