Skip to content

- Now with added high-frequency charts

- Up-to-date snapshot of the most important flows & liquidity metrics

- CB liquidity vs multiple markets

- Private vs central bank credit

- Mutual fund+ETF flows

- CB balance sheet details

- Our favourite US capital flight chart analytics

- Updated as of date above

- Valuation & positioning metrics for USTs, USD and gold

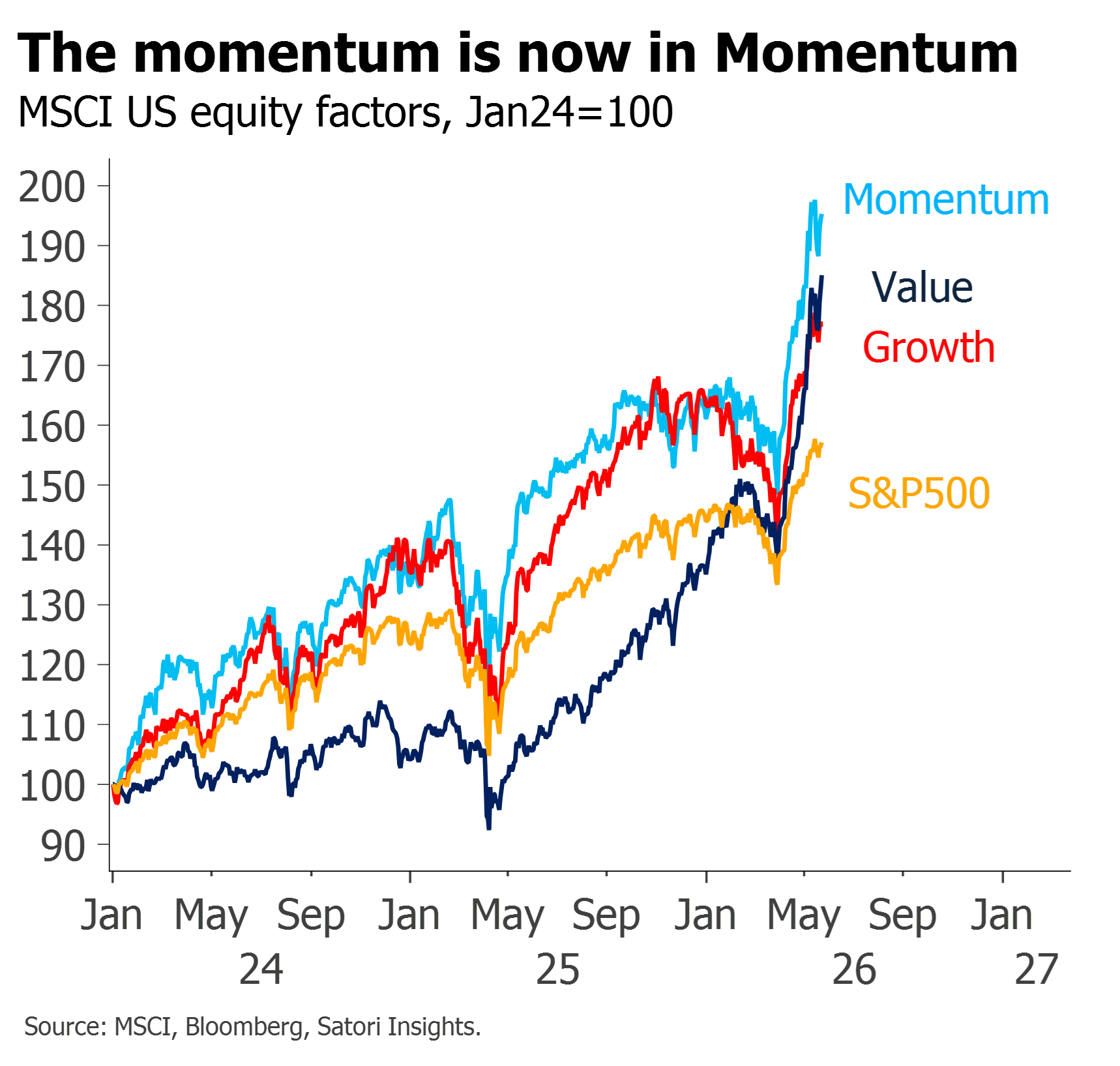

- Multiple markets are in melt-up – and for fifteen years, momentum has trumped mean reversion

- This feels instinctively unhealthy, and rightly so: crowding and herding really are at extremes across asset classes

- But it is not the sell signal it seems – neither for indices, nor for Momentum itself

- What crowding changes is the tail, not the trend: the real risk is a correlation spike

- The outlook for AI continues to dominate markets

- But the best insights come from first-hand experience

- This piece is free to view

- Full replay of 28 Apr webinar

- From oil above $120 to a Fed Chair who can’t trust a “closed” investigation, short term is driven by war and whim

- But the slide towards lawlessness is structural — not just Trump, not just populists

- Investors keep wanting to assume continuity in a world where the rules themselves have become negotiable

- First 15 minutes free to view; full version only for clients with Group Webinar and One-on-one subscriptions

- Free clip from 28 Apr webinar

- From oil above $120 to a Fed Chair who can’t trust a “closed” investigation, short term is driven by war and whim

- But the slide towards lawlessness is structural — not just Trump, not just populists

- Investors keep wanting to assume continuity in a world where the rules themselves have become negotiable

- First 15 minutes free to view; full version only for clients with Group Webinar and One-on-one subscriptions

- It’s not just the fog of war

- The drivers of lawlessness are structural

- Implications for investors

- The turmoil in markets says as much about positioning as it does

about stagflationary risks or the mercuriality of President Trump

- The immediate flight into $ cash reflects the unwind of active

positions

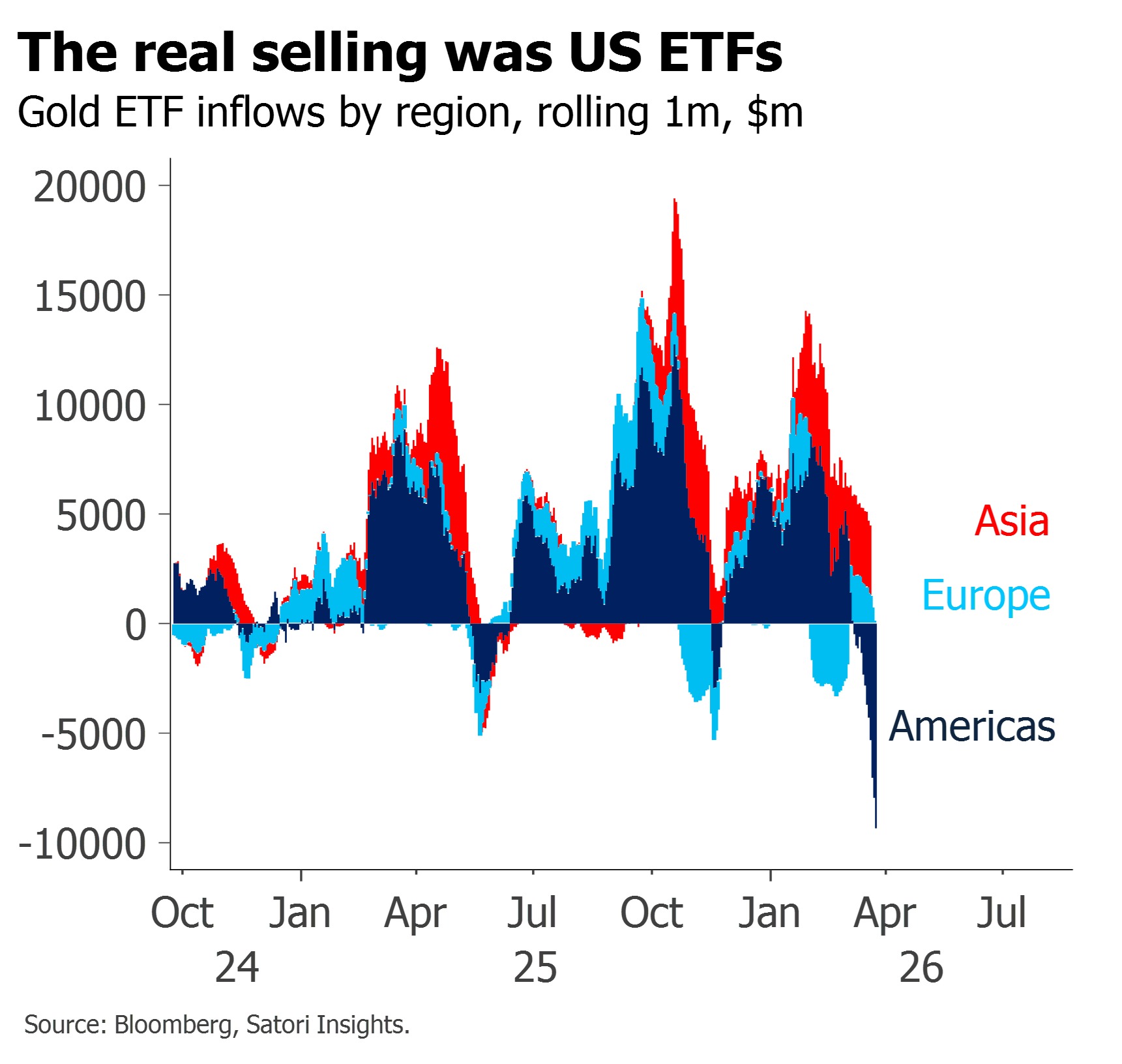

- But beneath the surface – and gold’s dramatic fall notwithstanding –

the US’ safe-haven status is visibly fraying