The significance of last week’s FOMC lies neither with the rate view, nor with the earlier, larger taper of QT – mildly bullish though both of these are.

It comes instead from the stark asymmetry of the response function which was described.

While the true test remains with the details of the liquidity outlook, in conjunction with the Treasury refunding this opens the door to a continued cross-asset rally through Q2.

The exuberance in risk assets is less a consequence of a stronger economy than a driver of it

The expectation of rate easing was never critical – which is why the exuberance has largely persisted even as yields have backed up

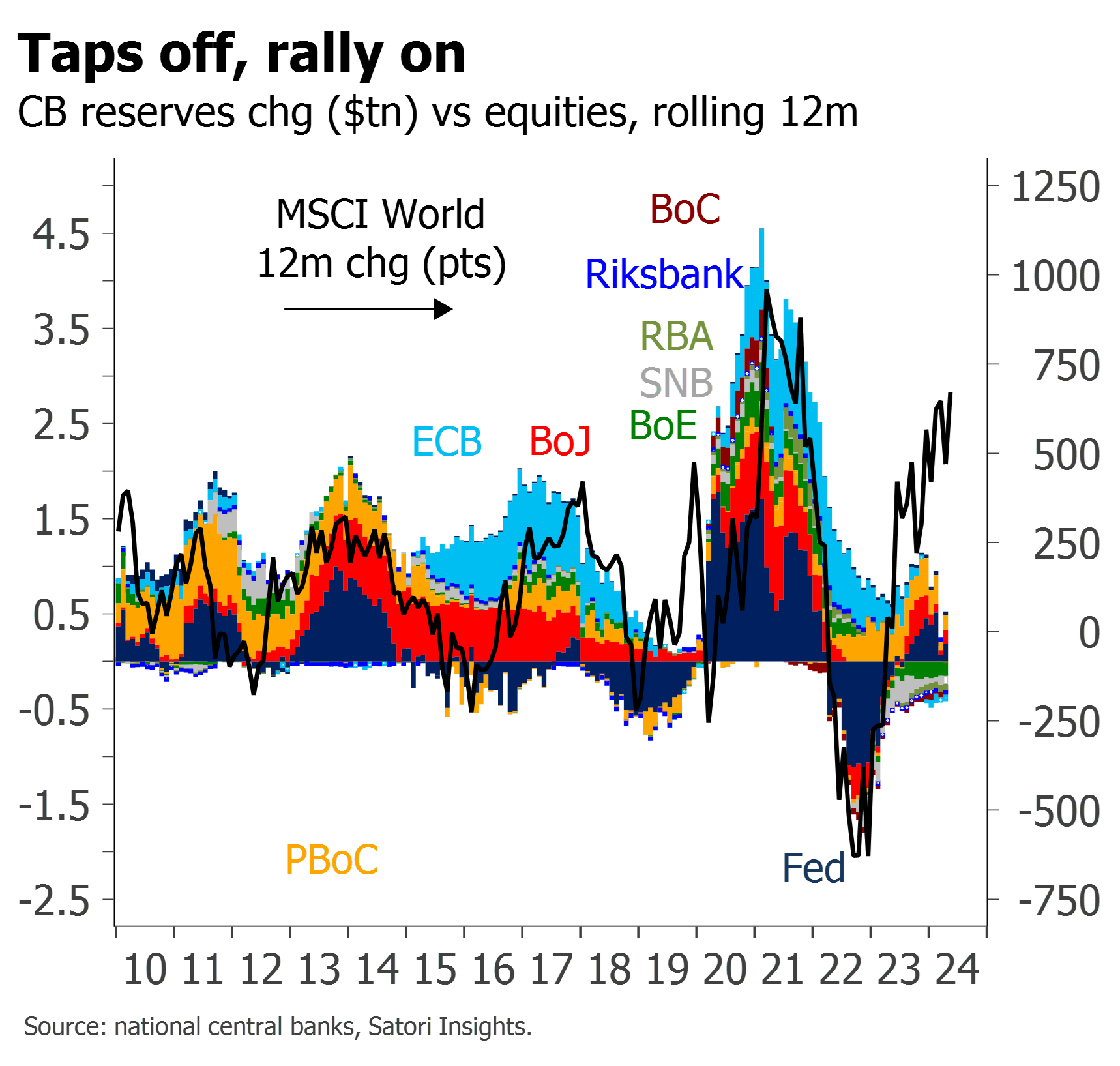

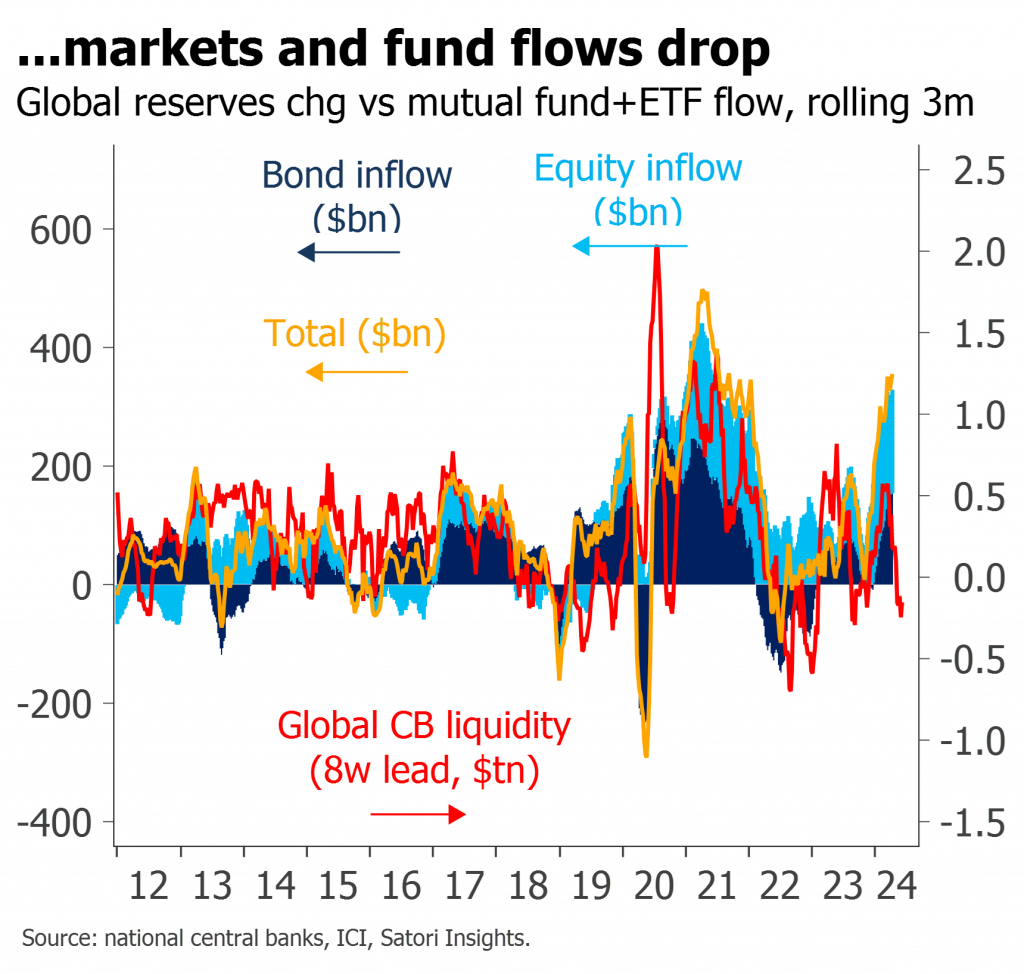

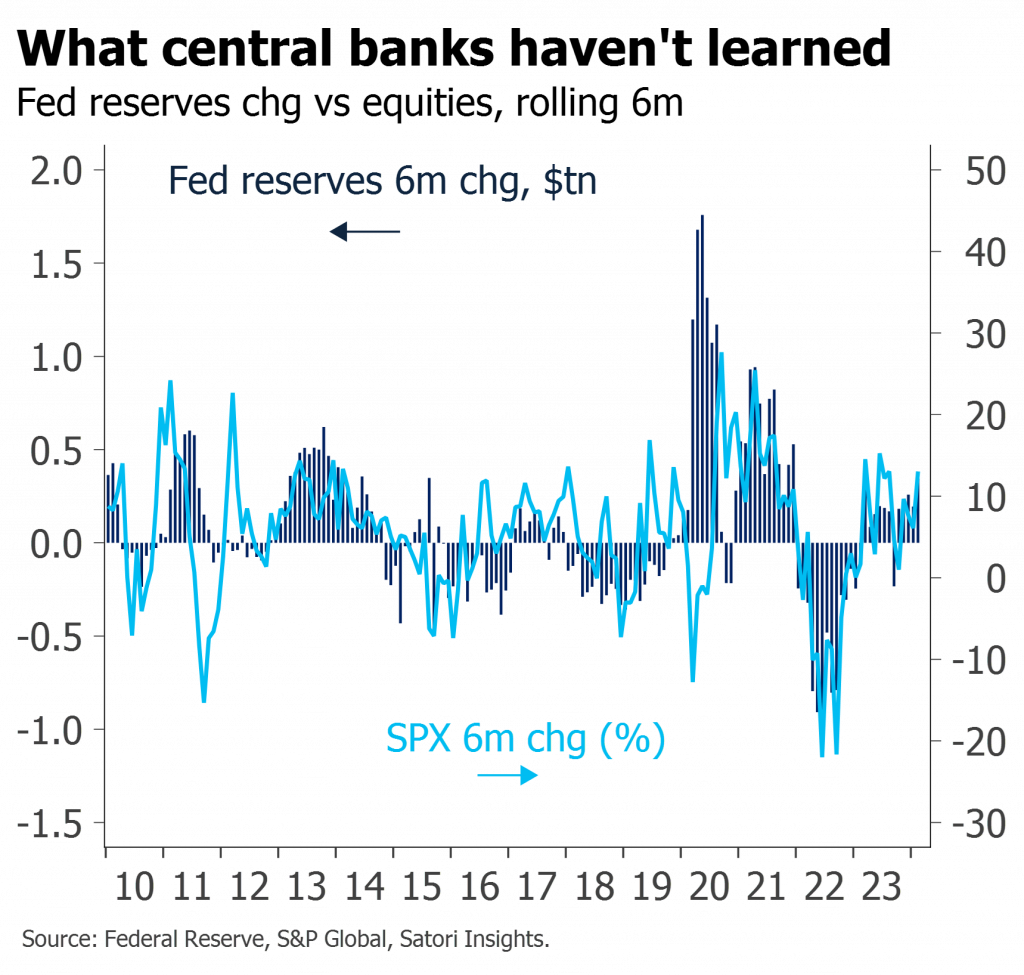

It is instead the direct consequence of investor crowding following easy central bank balance sheet policy – and vulnerable to any reduction in CB liquidity

The exuberance in risk assets is less a consequence of a stronger economy than a driver of it

The expectation of rate easing was never critical – which is why the exuberance has largely persisted even as yields have backed up

It is instead the direct consequence of investor crowding following easy central bank balance sheet policy – and vulnerable to any reduction in CB liquidity

Open to clients with Group Webinar or One-on-One subscriptions, and to the press