Skip to content

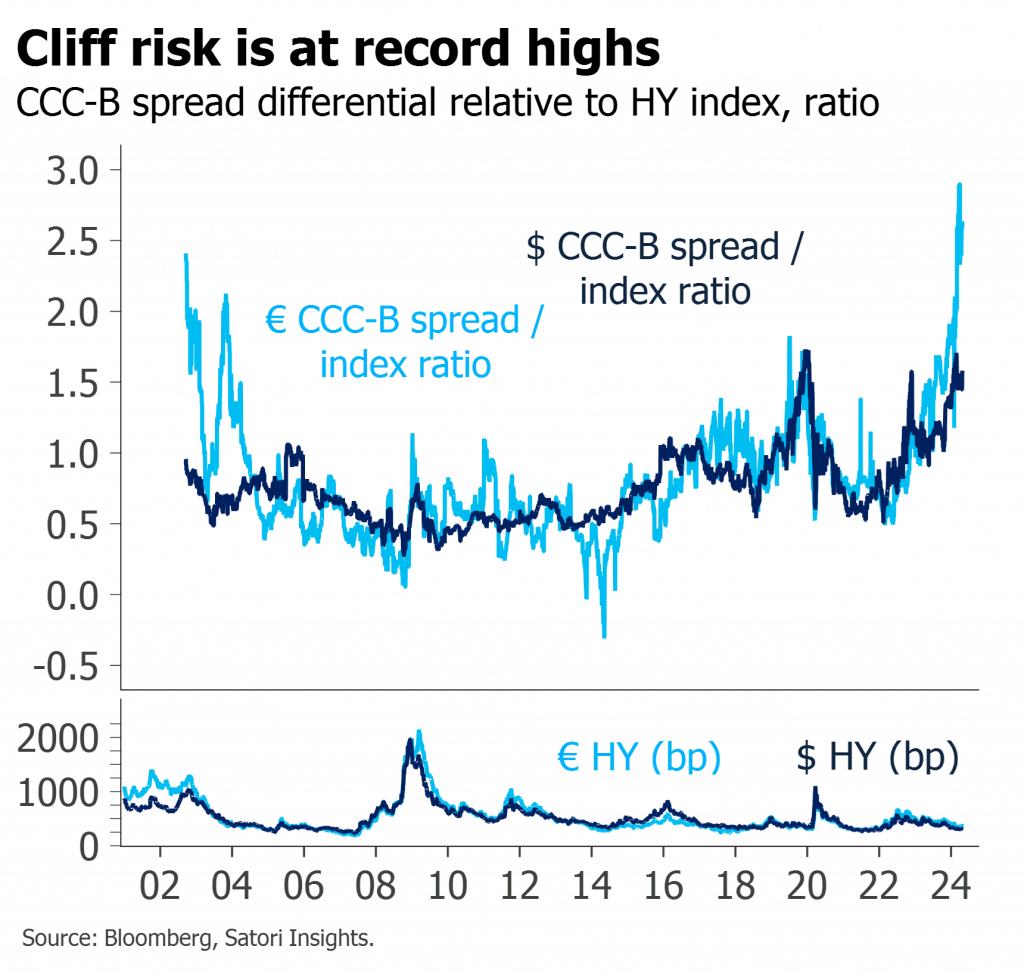

- Relative CCC cliff risk has risen to record highs

- This partly reflects hidden idiosyncratic risks from low recoveries and abandoned covenants

- But mostly it signifies the macro suppression of index spreads

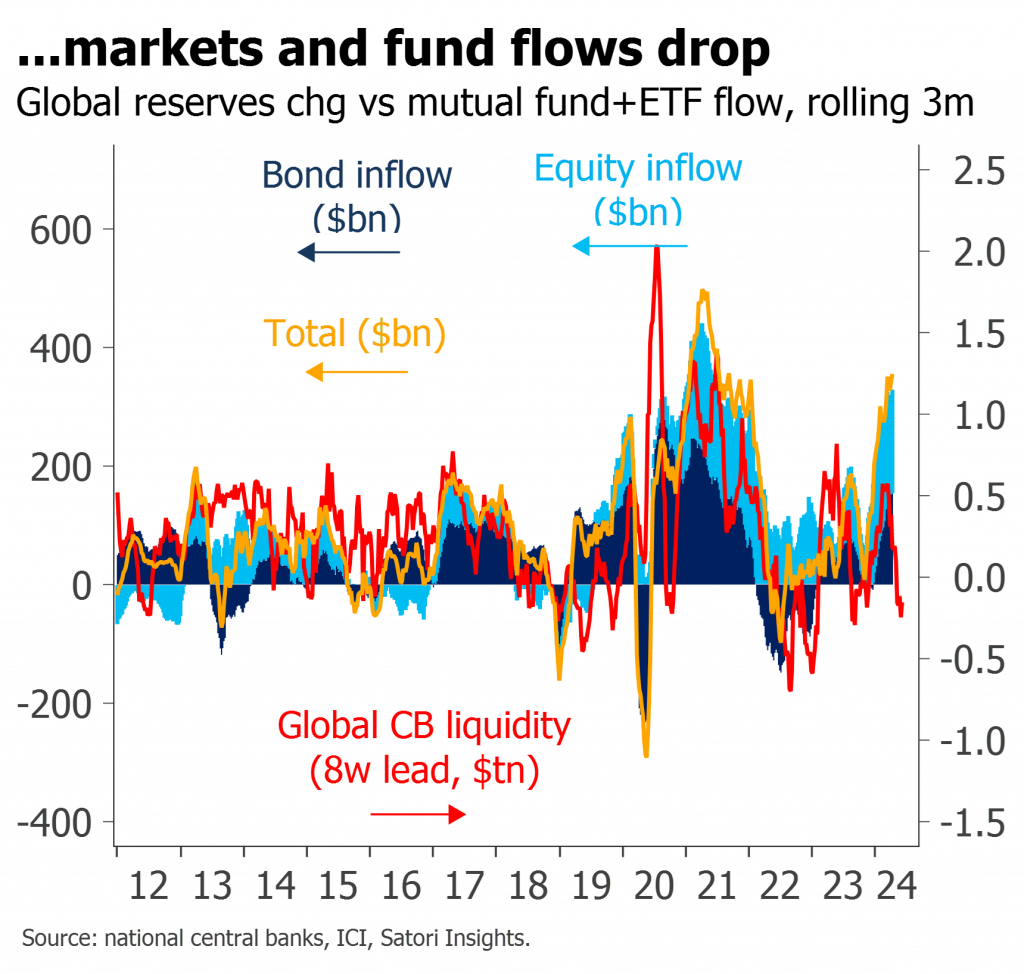

- The $280bn weekly drop in Fed reserves is the largest since Apr22

- Just as then, it coincides with a correction in markets

- A drop in fund inflows seems likely to follow

- But this still feels more like seasonal correction than decisive turn

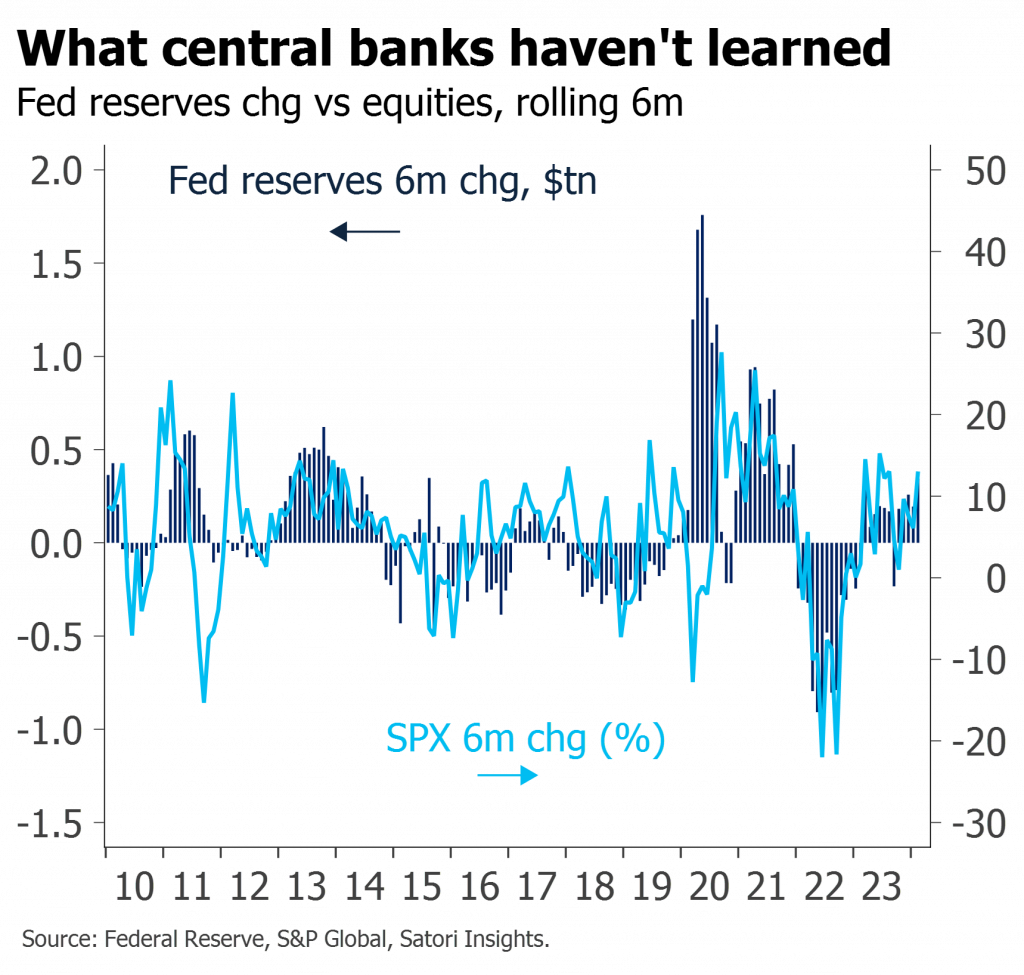

- Financial conditions have eased to the same levels as 2007

- This comes in spite of central banks thinking they are running restrictive policy

- The nature and timing of the market moves suggest these not so much reflect or anticipate the strength of the economy as drive it

- Their ultimate cause is easy balance sheet policy having crowded investors into risk

- Misunderstanding of these dynamics increases the likelihood of bubbles and subsequent busts

- The latest central bank research on QT is careful, rigorous, and grounded in the literature

- Unfortunately its main conclusion – that QE affects markets while QT doesn’t – is at odds with the lived experience of most market participants

- There is a much simpler reason why QT has had so little apparent impact

- Misunderstanding of this dynamic greatly contributes to the likelihood of future policy mistakes

- The rally in risk is often attributed to strong earnings

- But calendar earnings estimates have mostly been falling

- Macro drivers, not organic estimate optimism, are the true source of the markets’ strength

- After several months of liquidity tailwinds, risk asset pricing is starting to look excessive

- Improving spending, orders and hiring are all positives

- Despite this, earnings estimates are falling

- Fundamentals are reflective more of sticky supply than of dynamic demand

- Ongoing price pressures may well curtail central banks’ desire for dovishness

- But excitement about higher r* remains overdone

- Free-to-view replay of first segment of 16 Jan webinar

- Why strategists struggled in 2023

- A better way to think about markets

- Implications for 2024

- Full replay from 16 Jan webinar with Q&A

- Why strategists struggled in 2023

- A better way to think about markets

- Implications for 2024

- Open to clients with Group Webinar or One-on-One subscriptions, and to the press

- The remarkable performance of risk assets in 2023 is not primarily due to the growing likelihood of a soft landing

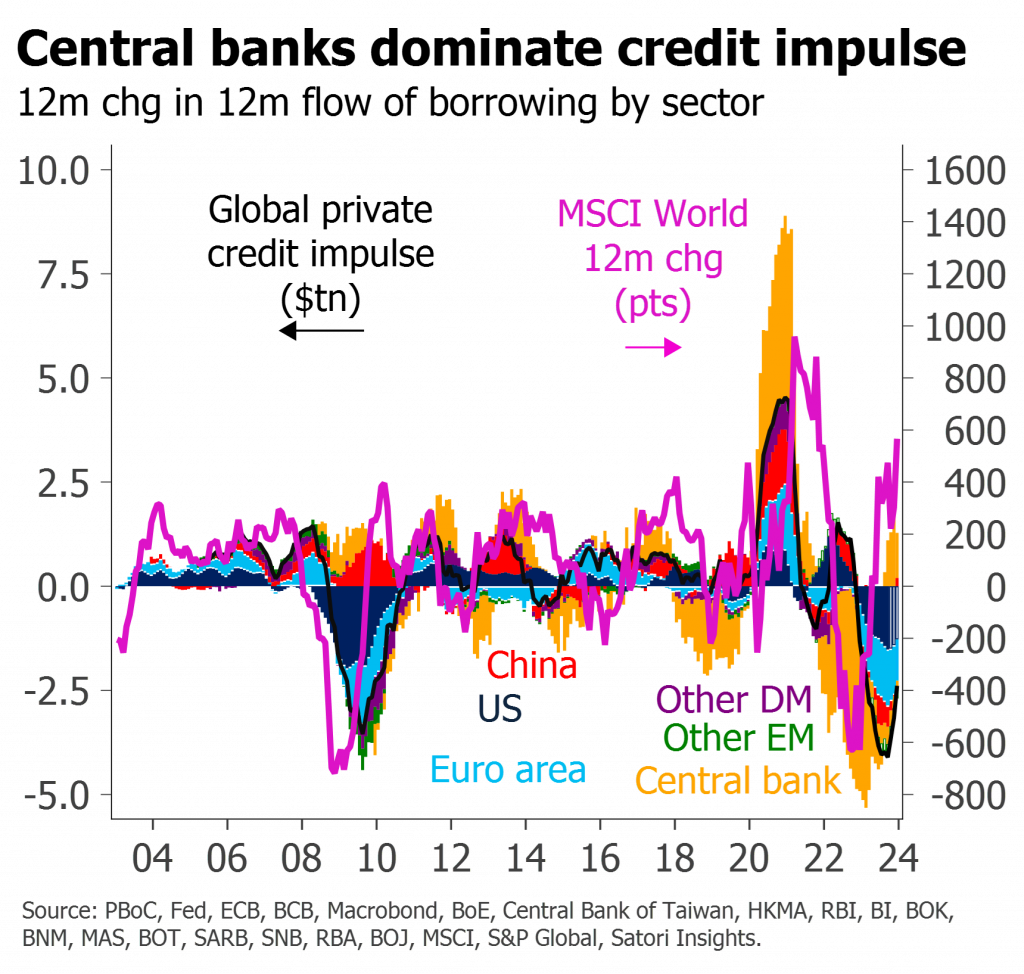

- It instead reflects markets being buffeted by extraordinary amounts of central bank liquidity

- For now, those technicals remain positive, but beyond Q1 they should fade or reverse

- Underlying momentum in growth, earnings and inflation – beyond sticky supply-side effects – is significantly weaker