Skip to content

- Free-to-view replay of first segment of 16 Jan webinar

- Why strategists struggled in 2023

- A better way to think about markets

- Implications for 2024

- Full replay from 16 Jan webinar with Q&A

- Why strategists struggled in 2023

- A better way to think about markets

- Implications for 2024

- Open to clients with Group Webinar or One-on-One subscriptions, and to the press

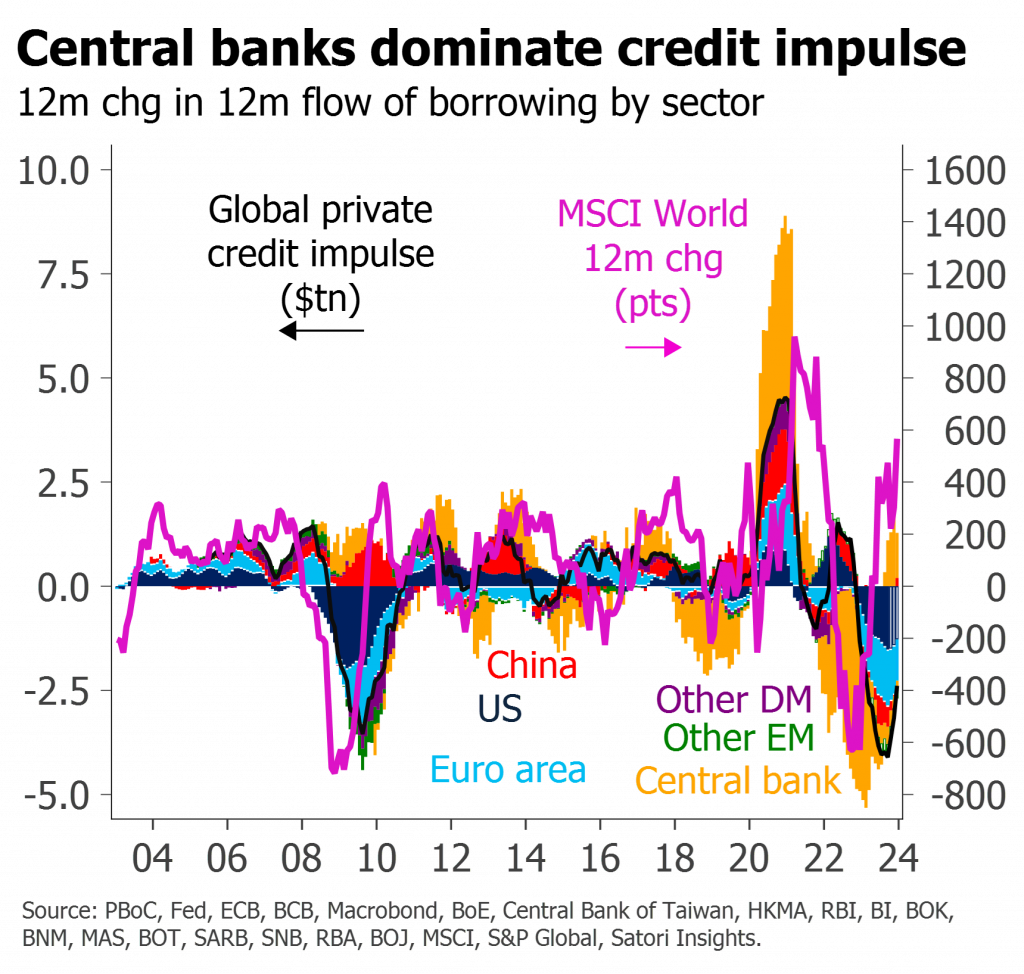

- The remarkable performance of risk assets in 2023 is not primarily due to the growing likelihood of a soft landing

- It instead reflects markets being buffeted by extraordinary amounts of central bank liquidity

- For now, those technicals remain positive, but beyond Q1 they should fade or reverse

- Underlying momentum in growth, earnings and inflation – beyond sticky supply-side effects – is significantly weaker

- Hark! The VC angels sing

- God rest ye, merry crypto bros

- While PMs watched tech stocks take flight

- I’m dreaming of a tight market

- To be sung, please, in a spirit of global harmony

- The biggest surprise of 2023 was not the resilience of the US consumer

- It was that central banks added nearly $1tn in liquidity, rather than removing $1tn as had been widely expected.

- This swing alone is worth 20% on equities – almost exactly the YTD gain in the S&P.

- We think 2024 will show central banks have overtightened rates whilst simultaneously overstimulating risk assets.

- But we also fear their misunderstanding of the dynamics means they may yet do more of both.

- The rally does not reflect the likelihood of a soft landing

- It is the direct consequence of a surge in Fed liquidity

- Widespread misunderstanding of these dynamics increases the likelihood of more rate rises and a harder landing later

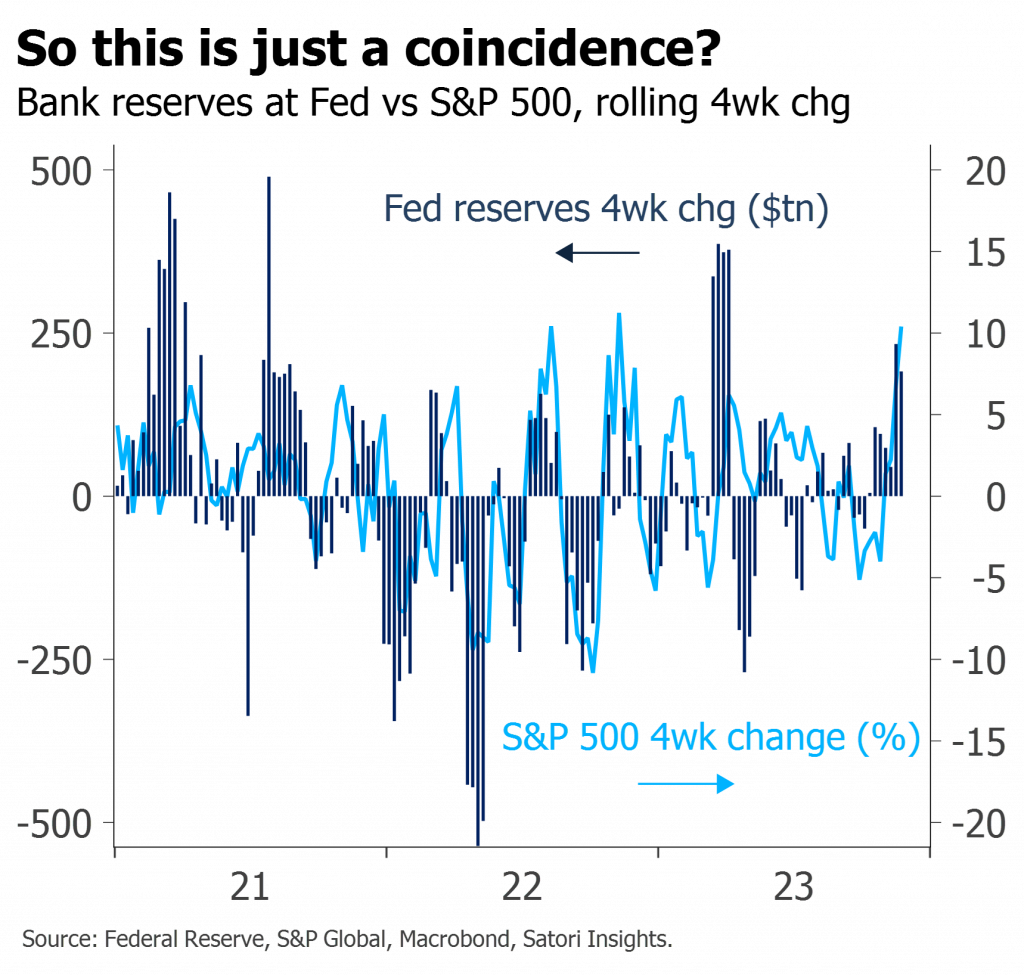

- Poor risk asset performance in Sep/Oct reduces gap to CB liquidity

- Fed $300bn reserve increase over past eight weeks helps explain renewed rally in S&P

- Conversely, despite talk of stimulus, China liquidity injections remain lacklustre

- Liquidity outlook still driven by RRP – and is much less negative than might be expected

- Persistent fiscal deficits are increasingly cited as the #1 reason to short bonds

- But the historical record is remarkably and perplexingly clear

- High debt levels, and even high fiscal deficits, have historically been associated with bond yields falling, not rising

- Only in part does this reflect factors like financial repression

- It is also due to the counterintuitive nature of the credit creation process itself